We've been covering YC batches as a quarterly snapshot of what technology makes possible. Time really flies; W26 still feels recent.

Venture capital moves in waves of interest. As an early-stage investor, YC makes bets on what it believes will be the next billion-dollar company, distributed across verticals, and you can see certain spikes.

YC is naturally leaning into new business models, partly inventing them, so the shift in expectations is worth watching. Customer support is the wave that just crested (F25 hit 11%); AI SDR was the 2024 wave. No one is even arguing that everything is about AI. The sentiment rhymes with the foundation-model collapse: build on models, not be one.

But no idea actually dies between batches, and it comes back more ambitious. The same startup keeps climbing toward owning more of the job as the base models get good enough to take the lower rungs.

TL;DR

- The dev-tools stack keeps rebuilding for AI agents: value migrated from the coding agent to the runtime around it.

- AI-native services keep rising, and the boldest stop selling software to an industry and become the provider itself: the insurer, the doctor, the customs broker.

- 13% solo founders (26 companies).

- Some new categories emerged in the batch: agent-trust-as-product, "company that runs itself" agents, infrastructure around prediction marketplaces.

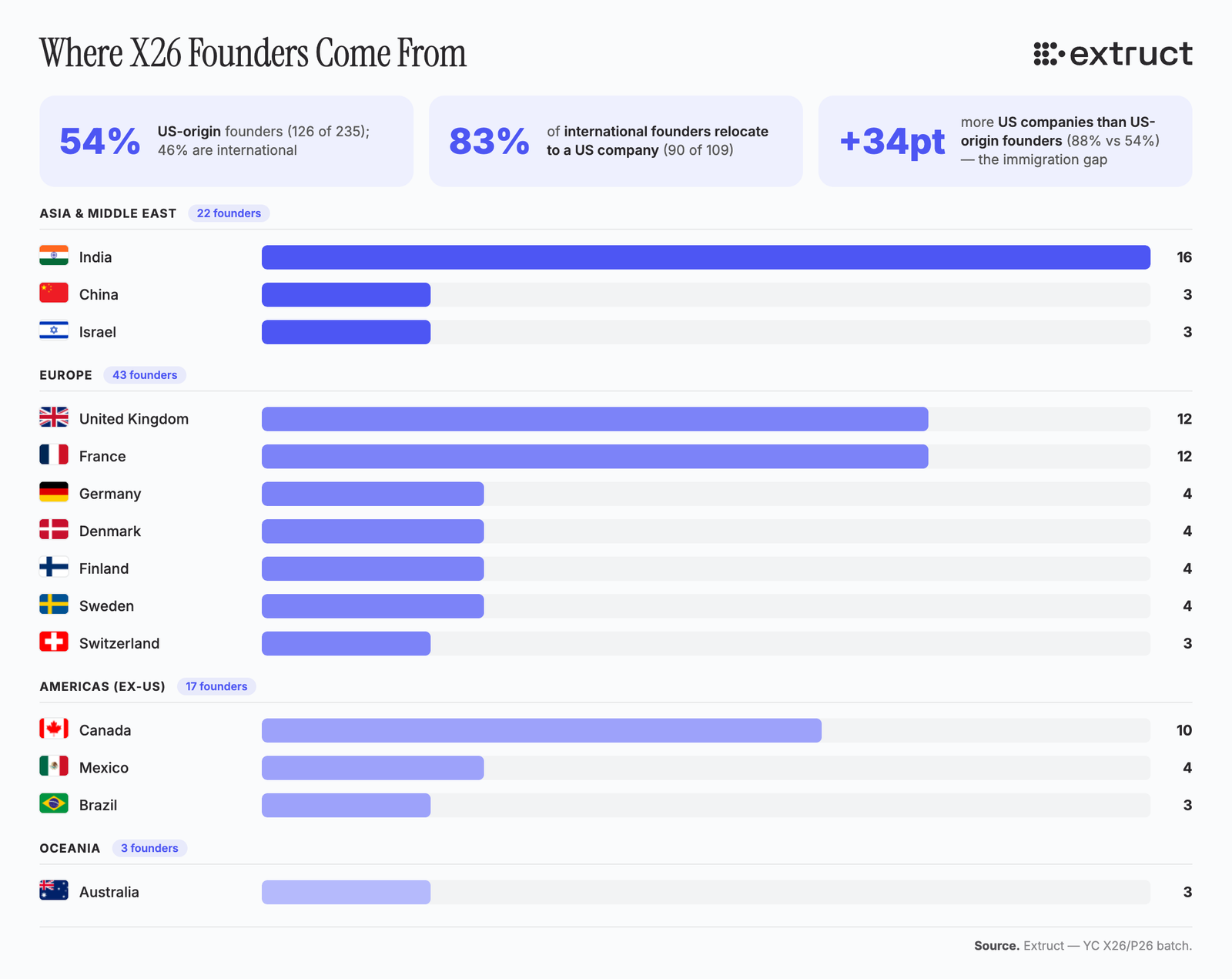

- Founders are global, but the companies aren't. 50% are of international origin, but 91% relocate to a US company. 13% build solo.

- The data supply chain is its own cluster. Startups manufacture the training data the web doesn't have, verifier-grounded examples, expert annotations, robot-demonstration video, and sell it to the frontier labs, who pay billions.

What they're building: ~205 companies

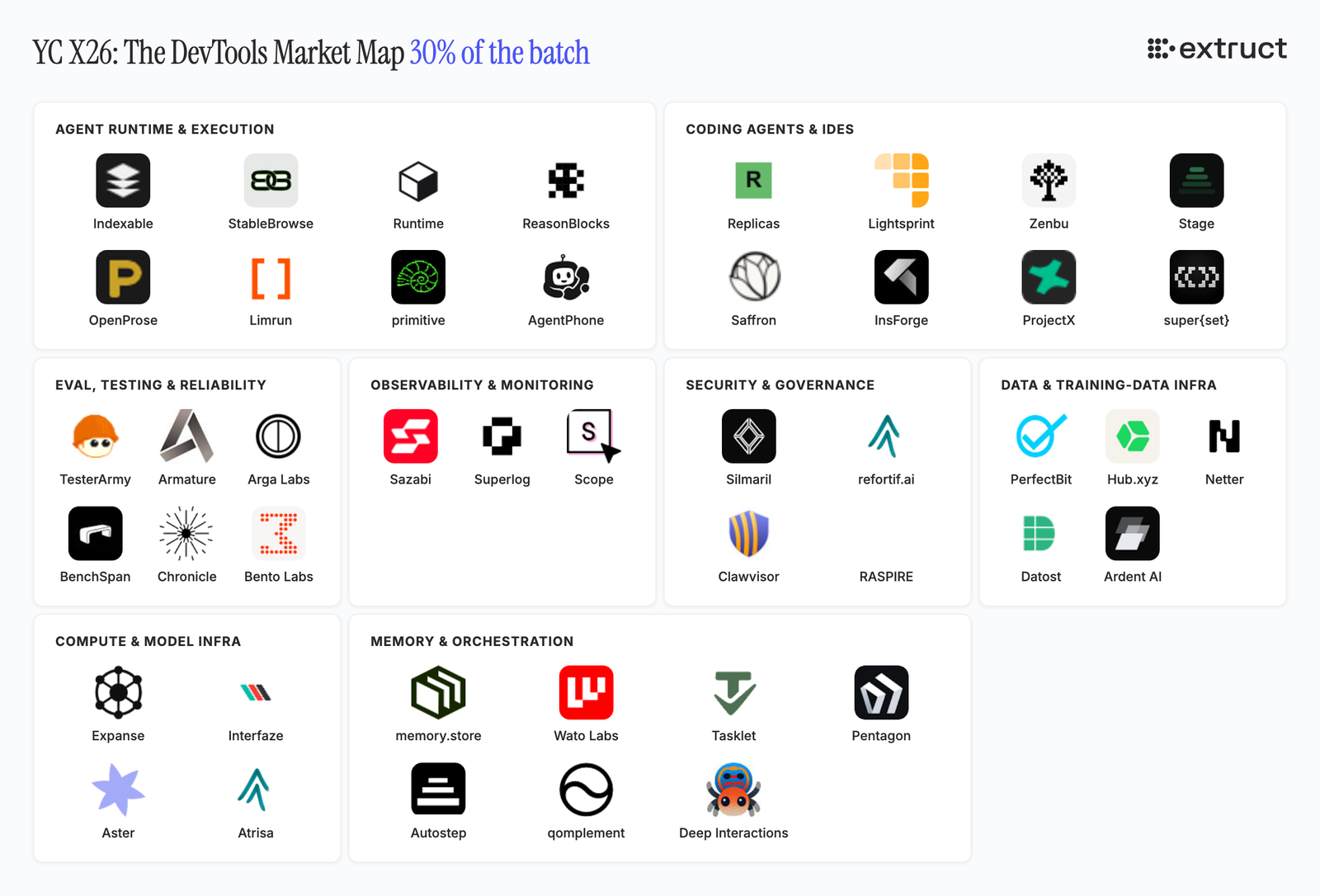

1. Dev Tools

Nobody's building another Cursor or Devin. But engineers are still the heaviest consumers of AI tokens, so the batch builds the layer around coding agents: run, test, verify, deploy.

Vibe coding accelerates feature development. That creates enormous bottlenecks upstream and downstream (security reviews, SRE, PMs). As the models got better at code, the startup's job moved from checking the model to running it unattended.

Startups building in that space: TesterArmy (browser QA testing), Armature ("test agent flows"), Arga Labs (code validation), BenchSpan (benchmarking), Chronicle Labs (backtest vs prod), Bento Labs (monitoring long-running agents).

On the other hand, agent infrastructure started as plumbing to wire models into tools. It became the hands agents act with (sandboxes, browsers), then the guardrails that stop them from breaking things, and now a trust layer that gates every action and even sells insurance on agent behavior (Mount, Klaimee). Each step responds to agents being trusted with more. So the frontier moves towards governance.

Some examples here: Indexable (sandboxes, 26ms fork), smol machines (virtual machines), StableBrowse (browser for agents), Zenbu (hackable interface for a coding agent), ReasonBlocks (runtime optimization that stops loops and failures), OpenProse (natural-language agent framework), Runtime (ship-with-coding-agents guardrails).

Another avenue is the data layer. The moat in AI labs moved to the data pipeline. The scarce input became data the internet doesn't have: expert annotations (worth 20–40× a crowd worker), verifiable RL environments, synthetic edge cases, and physical-world robotics data.

The batch's data companies walked exactly that path, from labeling existing media (Frekil) to manufacturing what was never online (PerfectBit's verifier-grounded data, Mantis's synthetic behavior). RL environments went from one company to a cluster. Robotics data is now the fastest-growing slice: human demonstration and teleoperation (Eden, Twolabs).

The irony: YC passed on Mercor in 2023 — the company that went on to define this category, supplying expert training data to the top labs at a roughly $10B valuation

Almost no frontier-model work (Aster = automated model training). But a few are working on compute/optimization: Expanse (HPC/GPU telemetry layer), Zibra Labs (HPC for quant backtesting).

2. Vertical SaaS aka "AI for X"

Frankly, I've stopped separating AI agents from the SaaS model; it's rare to see anything not AI at its core, so read these as vertical AI agents / AI for X.

The single most repeated shape is the "AI-native operating system for X," replacing the legacy vertical-SaaS incumbent.

Vertical SaaS, by industry:

- Healthcare (9): Harbor (AI-native clinical-trial software, auto-generates case report forms), Alchemy AI (image-analysis agent for labs), Klarify (auto-drafts therapy case notes), TakeCareOS (home-care and disability operations), Voquill (voice → pathology report), Enjamb (biopharma research app), Soria Analytics ("AI Bloomberg for healthcare"), Infera (plain-English lab protocols → workflows), Plena Health (clinical and revenue-cycle administration).

- Manufacturing / industrial / construction (11): Arzana (inside-sales order-execution system for manufacturing suppliers), Korso (agent: quoting, purchase orders, supplier comms), Prototyping.io (AI-native mechanical manufacturing), Dayjob (skip-hire scheduling), Smartbase (purchase-order entry from scanned orders), Pairio (industrial maintenance), Plan0 (preconstruction cost estimation), Rudus (concrete takeoffs), Hexa Agents (agents: sales, procurement, finance, service), Transload (3D dimensioning from CCTV), Walter (reads docs into ERP, 15 min → 1 min).

- Financial services (7): Kimpton ("IDE for investors"), Zolvo (lender servicing), Kinro (AI sales agents), Standard Signal (financial LLMs for autonomous trading), WithAI (automates investment research), Wealor (wealth-advisor app), Incandor (behavioral fraud).

- Legal / gov / compliance (5): Arden (SOX control testing), Complir (retail compliance), GovGuard (FOIA), Andco (case workups for plaintiff firms), Fuchsia (hardware-compliance agents).

- Blue-collar / real-world ops (4): Parrot (auto-shop back-office service), CentralComs (property-management voice), AquaShield AI (leak detection), Sidekick (SMS for deskless workers).

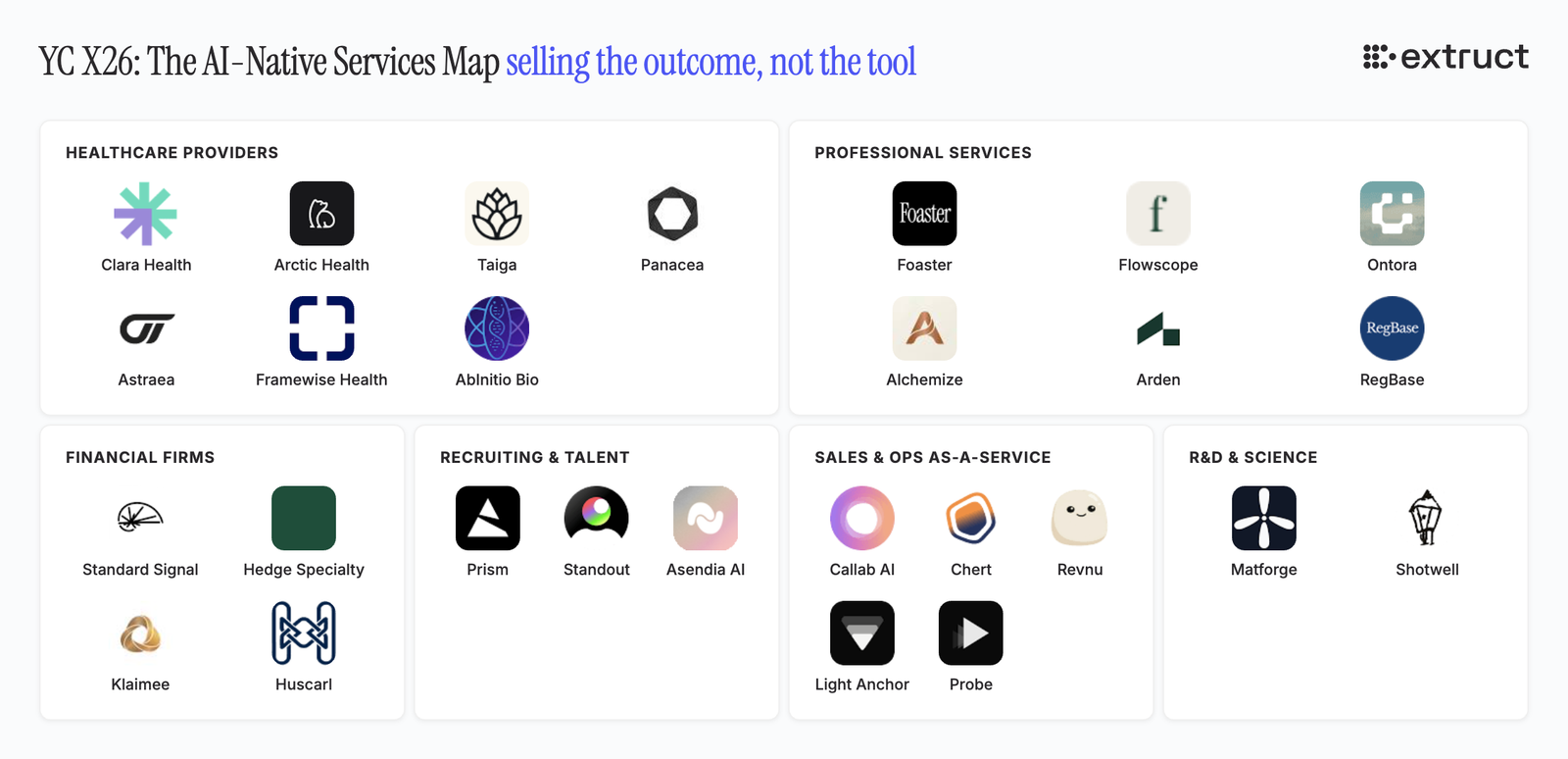

3. AI-native service: which professions AI is rebuilding

Plenty of companies brand themselves as an "AI agency" or "AI firm." The un-outsourceable work is the taste of defining the eval.

The big swing is rebuilding regulated, headcount-heavy services (insurance, billing, recruiting, consulting, primary care, brokerage) at software margins. The most aggressive become the licensed provider: Clara Health (doctor), Hedge Specialty (insurer), and Alchemize (customs broker). Licensed, regulated entity vs tool-for-the-provider is the real defensibility axis.

- Healthcare providers (5): Clara Health (AI primary-care doctor), Arctic Health (in-network credentialing), Taiga (medical billing), Panacea (FDA regulatory), Astraea (clinical-trial acceleration).

- Financial firms (2): Hedge Specialty (specialty insurance), Huscarl (actuarial).

- Professional services (4): Foaster (AI consulting), Flowscope (AI consulting), Ontora (management consulting), Alchemize (AI customs brokerage).

A related corner is forward-deployed engineers and system integrators. The un-outsourceable work is the taste of defining the eval. lab0 (AI forward-deployed engineers), Hessian (AI agents for business operations), Minicor (desktop automation), Gigacatalyst (embed into a customer's SaaS).

There are ~9 companies that brand themselves as a service but ship a tool: Prism (recruiting), Asendia (staffing), Callab (voice), Revnu (growth automation), Light Anchor (autonomous e-commerce), Probe (incident management), RegBase (regulatory tracking), Klaimee (agent insurance), Framewise Health (cardiac patient videos).

4. Growth Stack

Some ideas echo the previous batches, like Salesgraph and GojiberryAI.

The maximalist edge goes all the way: a company that runs itself. Thomas calls itself "the first AI founder, runs his own companies." The Company Company pitches "the last agent your company will ever need." Result wants to "build and run your companies." The product is the operator, not a tool the operator uses.

This is what makes the one-person billion-dollar company plausible. Solo founders are 13% of the batch (26 companies), and the pitch is that one person can manage an army of agents.

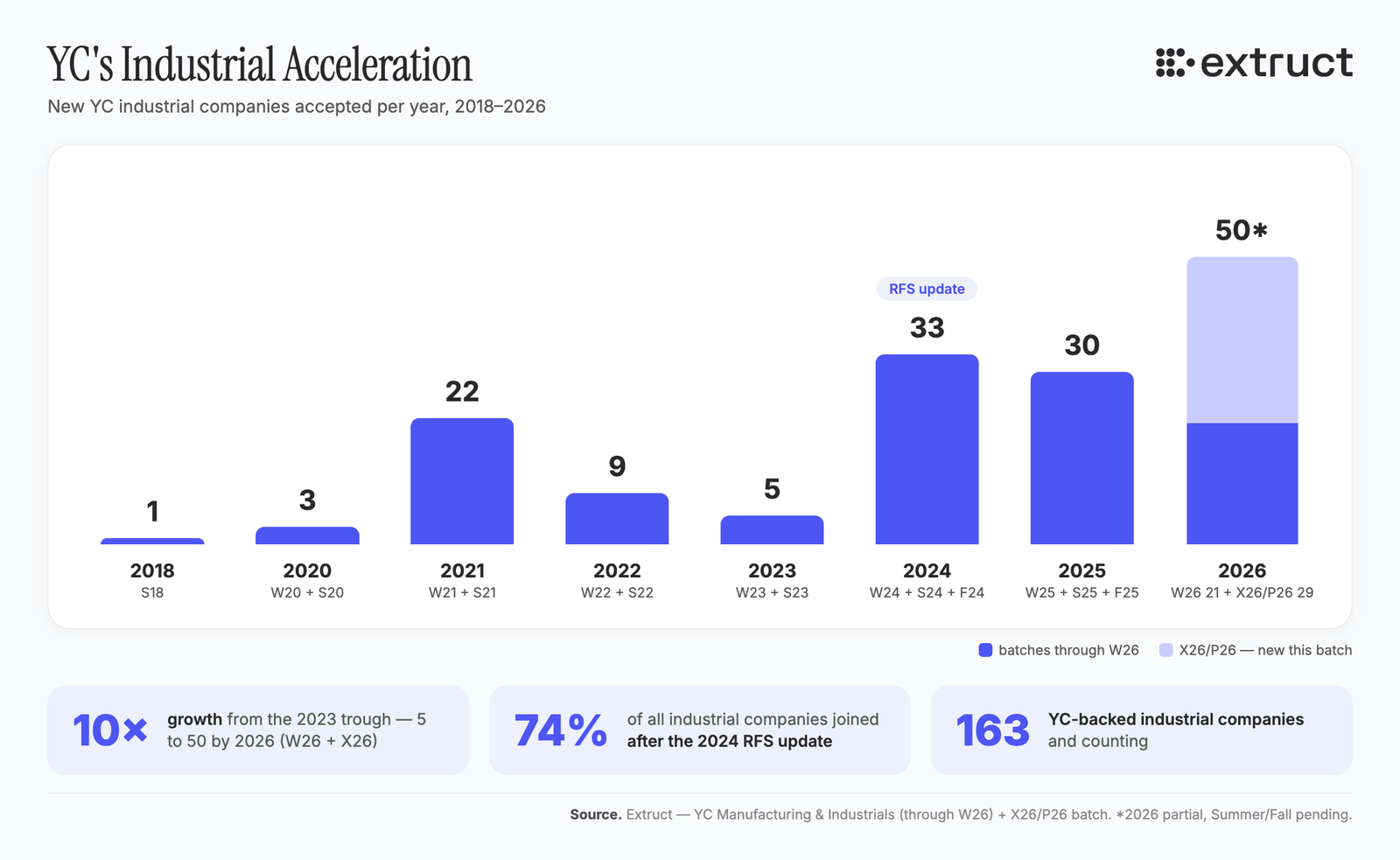

5. Hardware: where it's going

Hardware holds steady at ~10–11% of the batch, 22 companies shipping physical product. We track it every quarter, and the direction is now established rather than emerging. The center of gravity has shifted hard to defense. The bet is on cheap, mass-producible, attritable systems, built on the doctrine that many and cheap beats few and expensive. A $20K drone that forces a $4M interceptor breaks the other side's economics.

It's an arms race; the batch re-enters one rung higher. Offensive drone swarms drew a counter (shooting drones down), which drew missile defense, which has consolidated into software-defined counter-drone systems plus cheap, mass-producible strike drones (Tenet, Surtr).

9 Mothers (AI weapons), Maquoketa (autonomous drones Magpie UAS), Arlo (track drones/missiles), Surtr (counter-UAS), Ornadyne (surveillance bird-robots), Tenet ("F-150 for defense"), Nine Fives (RF test).

6. Prediction-market infrastructure

Like it or not — small but fast-forming, and worth separating: not the markets themselves, but the picks-and-shovels on top of Kalshi and Polymarket. It went from roughly one company in W26 to five in X26 — a bet that prediction markets become a real asset class, with the tooling forming around the two dominant venues the way agent-infra formed around the labs.

In a year, the batch built a full stack around them: a data feed (Dome), professional execution (River Markets), odds aggregation across venues (Oddpool), and a natural-language belief interface (Kassandre, by ValCtrl), with leveraged trading on the edge (Mochatrade).

7. Deep-tech (non-software, non-robotics)

Genuine deep-tech ≈ 18, strong technical-founder pedigree.

- Energy / nuclear / compute-power (aka Powering the AI Era): Apollo Atomics (most compact nuclear machines), Madrone (compute cooling), AICE Power (building-energy monitoring).

- Space / aero: Dispatch (orbital cargo-return, Free Flyer 1), Nine Fives (RF test; ex-SpaceX), General Aviation (ATC).

- Biotech / drug: AbInitio Bio (drug dev), Enjamb, Astraea, Adialante (mobile diagnostic MRI), Lumius Imaging (3D ultrasound; Duke), Juno (chronic illness), FinalDose.

- Materials / science: Matforge (semiconductor materials), Advanced Metal Research (welding).

8. Consumer

The batch is overwhelmingly B2B and infrastructure. Consumer is the smallest slice, about 13 apps (6%). It's a quiet corner, not where the batch is betting.

It hasn't really grown. Across the last five batches, the consumer has bounced between 4% and 10% of the cohort. So X26 is a small rebound in count (13 vs 9 in W26), not a new trend.

Personal finance is the small new wave. Health, wellness, and games stayed the anchor.

- Games and creators: Playabl (AI game builder), Pops (social game remix), YouArt ("Patreon for AI originals"), Clicky (Mac AI buddy).

- Personal AI: Ara (personal AI cloud), Jo (voice-first assistant).

- Personal finance: Gravy (personal AI CFO), Allowance (consumer agent wallet), Uno Wallet (rewards-card picker).

- Health and wellness: Imperfect (AI training coach), Juno (chronic-illness companion), NapkinMath (food diary).

- Home: Drafted (AI house plans).

9. Geography

76% of X26 is HQ'd in San Francisco (155/205). Then NYC (~11) and a thin US tail (Austin, Redwood City, LA, Seattle, Durham). Non-US (~10–12, Northern Europe-heavy): Complir (Copenhagen), Userlens (Helsinki), KugelAudio (Berlin), Transload (Munich), Tenet + Result (Stockholm), Dayjob/INTH/Prism/AgentPhone (UK).

Founder origins are far more global than the HQ map (traced by university and first jobs), 50% are US-origin and 50% international, led by the UK (33), India (29), France (21), Canada (17), Germany (14), Switzerland (10), and a 12-strong Nordic cluster (Denmark, Finland, Sweden). The UK pipeline is now bigger than India's.

91% of the international founders sit inside a US-HQ'd company; they relocate, the companies don't stay abroad. Angle: London, Paris, the Nordics, and the German/Swiss tier punch above their weight; everyone else moves to SF.

Conclusions

It's early to know how the moats shape up, and moats are overrated. But YC is betting on four, and the batch is already building each:

Compounding context. The system gets better the longer it runs inside your business. It learns your data, your exceptions, and your judgment calls. A rival starting fresh can't copy that. Savant sells exactly this, an operational-memory layer.

Orchestration reliability. In high-stakes work, getting it right 90% of the time is the same as wrong. The missing 10% is what blows up. Making an agent reliable enough to run unattended is the hard part, and that's the moat. Klaimee and Mount go further and sell insurance on it.

Workflow network effects. Once a tool becomes the place the work actually happens, everyone in the workflow has to be on it, and leaving gets harder. That's the Bloomberg effect. Soria wants to be that terminal for healthcare.

Trust in high-stakes domains. In regulated work, the right to act is the moat. No one lets an agent touch anything unless every action is gated, logged, and reversible. Clawvisor sits between agents and external tools and checks each call before it runs.