At Extruct, many of our customers use the product to search for companies in the industrial sector. The use cases vary: some search for metal forging suppliers, others source EPC providers who work the oil refineries, or look for US manufacturers producing golf vehicles.

It's great, but frankly, we never really had deep expertise in this space, so I spent last week exploring what's happening in the industrial and manufacturing landscape in the US.

My basic knowledge was that manufacturing in the US is still quite innovative despite all the negative narratives. Output has roughly tripled since 1975, even as employment fell from 19 million to 13 million workers. The modern political drivers are well-documented: tariffs, geopolitical realignment, and rising defense budgets. But I was quite surprised to see that real-sector tech is quietly climbing into one of the hottest investable theses of 2026.

So here's the research on startups rebuilding a modernized U.S. industrial base — the techno-industrialists who may raise trillions and extend U.S. prosperity well into the next century.

But first, a bit on "why now?"

- The US industrial base is dependent on thousands of "mom and pop" machine shops, with no single player owning more than 1% market share. Traditional "mom and pop" shops are like world-class custom tailors. They are brilliant at making one or two incredibly complex, "bespoke" items, like a single perfect hatch for the Space Station. In the 70s and 80s, U.S. manufacturers shifted from vertically integrated production toward specialized supplier networks under competitive and financial pressures. Thus, many large manufacturers stopped making their own parts and began outsourcing them to these small domestic shops. A single Boeing 747, for example, has 6 million parts provided by 20,000 different suppliers. These small shops were built to produce a few bespoke exquisite systems, rather than the high-volume "proliferation" (hundreds or thousands of units) that companies like SpaceX require. They need hundreds or thousands of satellites and drones. A custom tailor can't suddenly start sewing 10,000 uniforms a day without a totally different system.

- Most factories still run on systems designed in 1995. Legacy spreadsheet infrastructure is collapsing under complexity. These shops often use PDFs and spreadsheets to track serial numbers, revisions, and load balancing. Automation would help, but hiring software engineers rarely pencils out, both economically and culturally.

- High-skill trades take decades to master, and even basic electrician certification requires a five-year apprenticeship. The average industrial worker is 55 years old; the average owner-operator is 62-63. Most factories have no succession plan. Instead of being sold or handed down, many owners simply "sunset the business and lock the door" or, at best, get consolidated into roll-ups when they retire. Because of a cultural shift where manufacturing is no longer seen as "sexy" or high-status (but that is changing - read more below), the children of these operators frequently pursue college degrees and office jobs rather than taking over the family trade. Most of these manufacturers rely on "wizard-like" tribal knowledge, undocumented expertise held in the heads of a few individuals.

Traditionally, we treat YC companies as a good proxy for VC interests, so I decided to start there.

What YC Wants Founders to Build

In February 2024, YC published its first RFS update since 2018, listing 20 categories it wants to fund. Seven directly target the physical world: robotics, physical world simulation, defense tech, manufacturing reshoring, space, Modern Metal Mills (software-defined systems to rebuild mills).

Well, yes, you read it right - YC is explicitly asking founders to own factories.

While founders in SaaS argue on LinkedIn about whether the data or UX layer provides the strongest moat, OG hardware founders understand that real moats and $T in TAM lie in government contracts with 5-10 year procurement cycles.

Three Business Models

YC's industrial companies fall into three distinct categories, each with radically different business models, capital requirements, and defensibility moats.

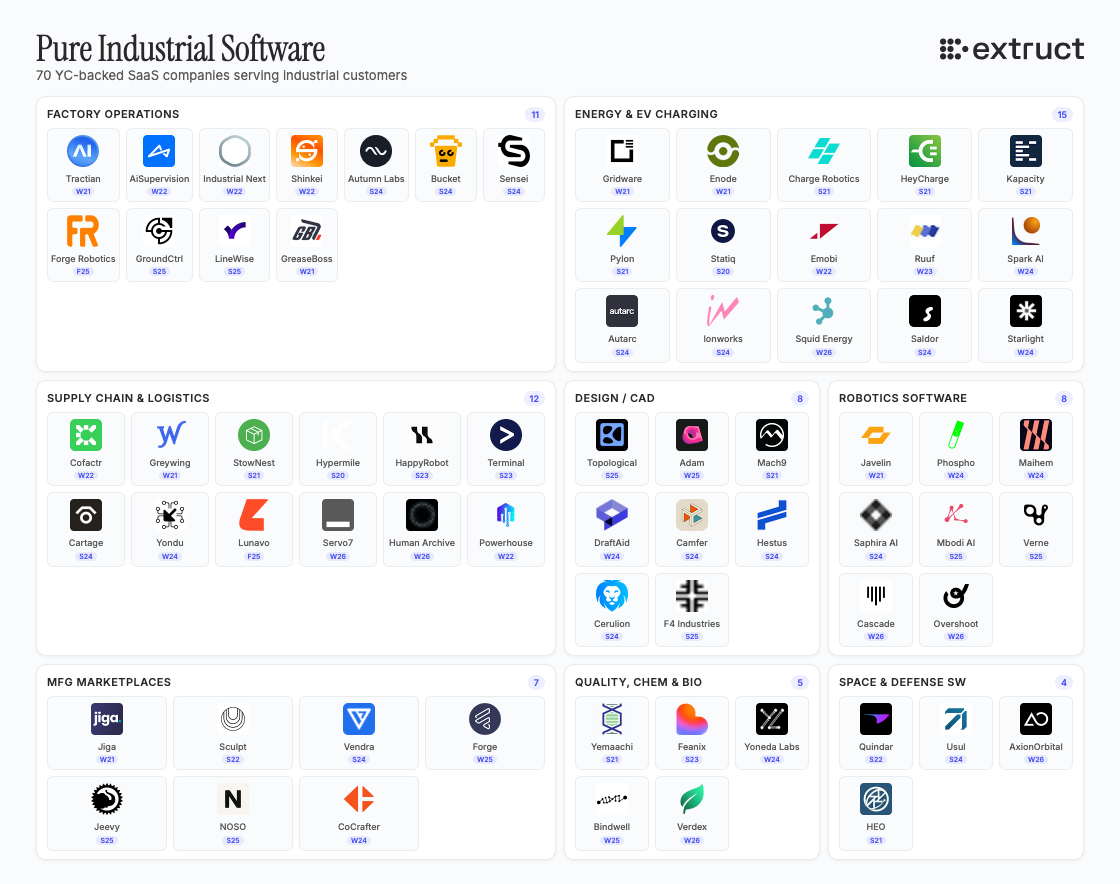

Model 1: Pure Industrial Software

These are pure-play software companies serving industrial customers. Low capex, high margin, classic SaaS economics, but with industrial switching costs.

Some companies that we feel quite excited about:

Factory Operations

- Autumn Labs (S24): Datadog for industrial robots, real-time monitoring across factory floor equipment

- Industrial Next (W22): Tesla-style autonomous manufacturing for everyone

- HappyRobot (S23, $44M Series B): AI voice agents automating freight and factory logistics

- Tractian (W21): Industrial asset intelligence platform

- Bucket Robotics (S24): AI-powered defect detection

Energy & Grid

- Gridware (W21, $55M growth round): Wildfire prevention through real-time grid monitoring

- Starlight Charging (W24): 10x cheaper EV charging for apartments and condos

- Autarc (S24): AI-powered energy management for buildings and industrial sites Ion Works (S24)

Supply Chain & Logistics

- Cofactr (W22, $17.2M Series A): Electronic component supply chain intelligence

- Corvera (W26): Supply chain orchestration for CPG brands

- Vooma (W23, $13M Series A): AI agents automating order entry and freight quoting for logistics companies

Design & CAD Tools

- Topological (S25): Physics-based CAD optimization, 1930x faster than current methods

- Adam (W25): AI-powered CAD that generates production-ready designs

- Diode Computers (S24, $11.4M Series A): Circuit board design AI

Quality & Compliance

- GroundControl (X25): FAI, PPAP, AS9102 compliance automation

Chemical & Materials

- Yoneda Labs (W24, $4M seed): AI-driven optimization for chemical reactions

Manufacturing Marketplaces

- Vendra (S24): Marketplace connecting buyers with verified US manufacturers Jiga (W21)

SaaS can certainly improve efficiency in real-world businesses, but it's hardly designed for fundamental changes. Good software matters but not sufficient.

Model 2: Software-Defined Factories

Every strong thesis has a predecessor that was a bit "early" coupled with wrong execution. In 2015, Jeremy Herrman and Nick Pinkston were hosting hardware meetups in cities around the globe and realized they were hearing the same complaint over and over: it was difficult for hardware entrepreneurs to find manufacturers willing to take on their projects. So at the beginning of 2014, the two launched Plethora, a fully vertically integrated factory in the neighborhood of San Francisco, filled with advanced 3D printers, and raised $35 million from top funds.

But the customer demand for high-precision parts wasn't there yet, and they also tried to do everything in software, cutting humans out of the loop entirely, which meant years of wasted time trying to solve the problems that humans could easily handle.

Hadrian (Series C - June 2025; total funding $730m) took a different approach. Founder and CEO, Chris Power, started by selling software to machine shops. The lesson was brutal: you can't bolt modern software onto a factory running systems from 1995 and expect transformation. The factory itself has to be the product.

So Hadrian built three software layers from scratch: DFM (design for manufacturability review), CAM (automated machine programming), and Flow (real-time production scheduling). Think Tesla Gigafactory or SpaceX Starbase, where the production lines are "software-oriented." The result: Hadrian trains retail workers to produce aerospace-grade precision parts in 30 to 60 days, instead of the years it would normally take. That's the key shift, not "software on top of a factory," but the factory re-architected around software from day one.

Taking this inspiration, YC companies are aiming to digitize the "primitives" of manufacturing - modernizing this supply chain by building a network of vertically-integrated advanced manufacturing factories.

Just as AWS allowed software developers to rent server capacity instead of building data centers, these companies want to provide the "building blocks" so next-generation entrepreneurs can focus on product design and R&D rather than factory construction.

All of this should translate into strong margins. Chris Power from Hadrian noted that top legacy space and defense machine shops generate ~30-40% gross margins, and modern tech-enabled manufacturers can earn 50% gross margins.

YC-Backed Factories:

- Atomic Industries (W21, $25M Series A): AI-powered precision manufacturing for aerospace and defense

- Daedalus (W20, $21M Series A): Automated CNC machining for high-mix, low-volume parts

- RMFG (S21): Software-defined sheet metal factory

Most companies in high-mix manufacturing (a wide variety of different, highly specialized parts in relatively small quantities) follow a model built around producing a wide variety of highly specialized parts in small quantities.

The caveat, you need to be a GOAT fundraiser to pull this off.

Many investors don't understand how manufacturing businesses scale and try to apply successful software growth metrics to manufacturing operations.

To avoid massive dilution of equity, companies like Hadrian use a split financing strategy - VC should fund the compounding advantage (automation, AI, software systems), while debt finances the fixed assets that can be collateralized (heavy factory equipment and physical infrastructure).

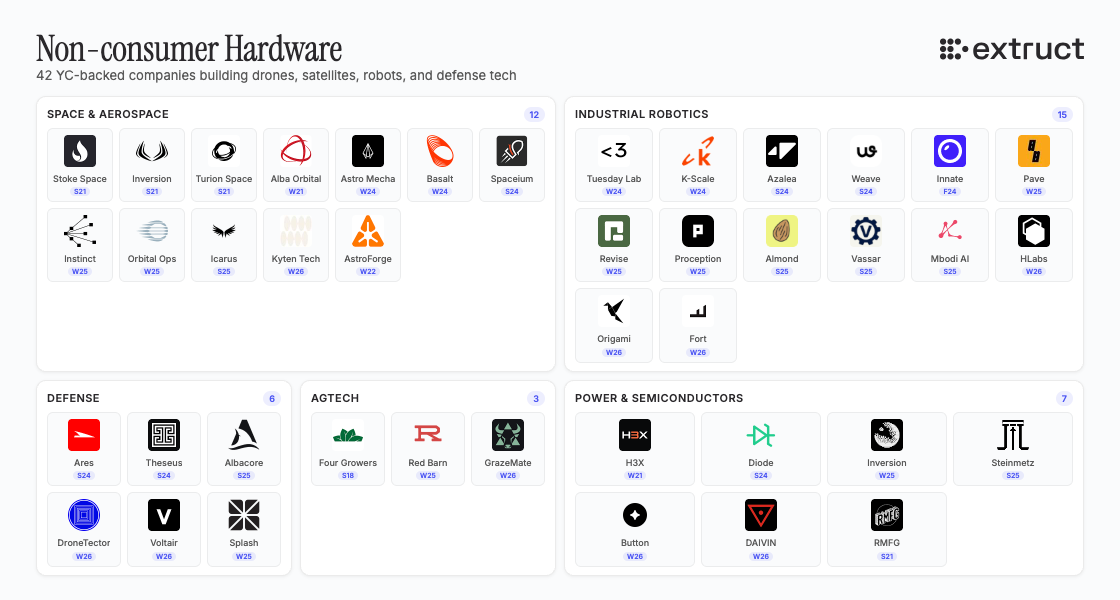

Model 3: Non-consumer Hardware

A drone, satellite, or robotics company does not say "we are a manufacturing company", they say "we specialize in drones, satellites, or robotics." Why? Because using "manufacturing" in your billing signals heavy capex and negative optics.

But beneath the surface, all these companies face the same challenges: substitution of labor, tribal knowledge evaporation, and the marriage of software with physical production. They're all potential customers of Model 2 software-defined factories.

Robotics:

Robotics has been around for some time, and now with AI, there is suddenly a bunch of hype.

- Shinkei Systems (W22, $22M Series A): Automated fish harvesting at sea

- Four Growers (S18, $9M Series A): Autonomous greenhouse harvesting robots

- Maihem (W24, $6M seed): Adaptive AI robots for industrial tasks

- Bindwell (W25, $6M seed): AI-driven pesticide discovery

- Forge Robotics (F25): AI-powered welding automation

- Pivot Robotics (W24): Autonomous grinding and surface finishing

- Verne Robotics (S25): Intelligent robotic systems for industrial automation

- GrazeMate (W26): Autonomous livestock management

- Azalea Robotics (S24): Automated airport baggage handling

- Origami Robotics (W26): Foldable robotic systems for confined spaces

- Phospho (W24): Open-source robotics development toolkit

- Sensei Robotics (S24): Scalable robotics training data collection

- AutoPallet Robotics (S24): Ceiling-mounted autonomous mobile robots

- Kyten Technologies (W26): Aerospace-grade battery pack manufacturing

- Revise Robotics (W25): Automated electronics refurbishment

Motors & Power:

- H3X Technologies (W21): Ultra-high-performance electric motors for aerospace

- Steinmetz Motors (W25): Next-gen EV motor controllers

Space:

Commercial space is seeing a massive capital influx, making it the ideal entry point. These companies are often run by younger leaders (30-year-olds vs. 50-year-olds) willing to take a shot on a new manufacturing platform and pay a premium for speed.

- Stoke Space (W21, $860M Series D): Fully reusable rocket

- Inversion Space (S21, $44M Series A): Orbital delivery and re-entry capsules

- TransAstra (S21, $27M): Orbital logistics and asteroid mining

- Quindar Space (S22, $18M Series A): Automated satellite operations platform

- Spaceium (S24, $6.3M seed): In-space refueling with $86.1M in binding contracts

- AstroForge (W22): Asteroid mining and space resource extraction

- Orbital Operations (W25, $8.8M seed): On-orbit satellite servicing

- Reditus Space (W25, $7.1M seed): Zero-gravity manufacturing in orbit

- Basalt Space (W24): Operating system for satellite constellations

- Alba Orbital (W21): Ultra-small satellite manufacturer

- HEO Space (S21): Non-Earth imaging for space domain awareness

- Cascade Space (X25, $5.9M seed): Deep space communications infrastructure

- Instinct Space (W25): Lunar GPS navigation system

Defense:

Defense manufacturing went 10x in three years: $500M (2022) to $4.7B (2025). Pentagon spending surged, but 54% of the $4.4T defense budget still flows to legacy primes (Lockheed, RTX, Boeing). Less than 1% of contracts go to venture-backed startups despite $35B in VC funding.

- SalesPatriot (W25, $5M seed): Defense procurement platform with $200M+ in Pentagon contracts

- Albacore Inc. (S25, $6.5M): Autonomous undersea vehicles

- Ares Industries (S24): Low-cost cruise missiles

- Usul (S24, $3.3M seed): AI-powered contract capture for defense

- Splash Industries (W25): Autonomous patrol boats

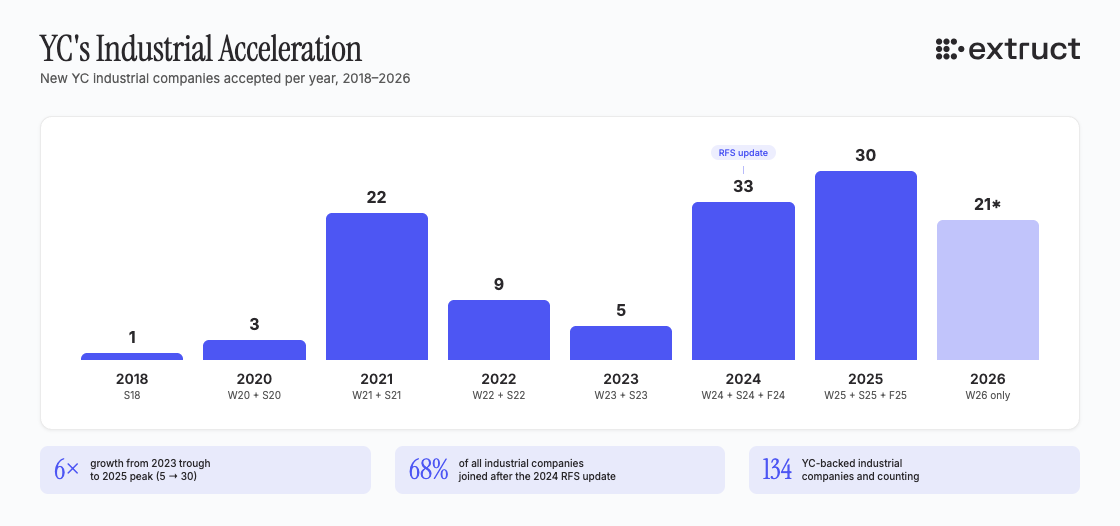

The Talent Shift

The numbers tell the story: YC accepted 18 industrial companies in 2021, then just 3 in all of 2023. After the February 2024 RFS update explicitly calling for factory founders, the floodgates opened, 21 in 2024, 24 in 2025, and W26 is already at 21 as the batch wraps up.

The most significant impact of YC's industrial push is getting software engineers excited about automating manufacturing again, drawing elite talent away from building a GTM tech SaaS or trading corn derivatives in a hedge fund.

But founders alone aren't enough, a Deloitte survey found 47% of Gen Z express interest in manufacturing jobs, but 62% want clearer career paths first.

We may get to the point where a factory runs like a SaaS company with a production capacity you can point at whatever the world needs next. But physical systems still generate irreducible ambiguity — and that's where technician expertise compounds.

Non-Consumer Hardware Represents ~15% of YC W26

The trend is accelerating. In the current W26 batch, non-consumer hardware companies account for roughly 15% of all accepted startups — a significant share for a category that most accelerators still ignore. This isn't a niche anymore; it's becoming a core pillar of YC's portfolio strategy.